Where AI infrastructure bottlenecks may reshape value

AI Infrastructure · Consensus Stress Test · June 2026

SignalScope View

Most market commentary has moved to the same conclusion: AI needs more power, chips, data centres and cloud infrastructure.

That is now the consensus.

The more important question is what comes next. Which constraints create durable advantage? Which create execution risk? And which companies can actually turn AI demand into deliverable capacity?

AI infrastructure advantage may not sit with whoever has the loudest demand story. It may sit with whoever controls the scarce inputs that make AI usable: power, chips, cooling, sites, finance, regulatory permission, trusted data and governed deployment.

The market has noticed the constraint. It may not yet be underwriting the quality of deliverability.

The demand story is no longer enough

AI adoption is accelerating. Hyperscalers are increasing capex. Specialist compute platforms are raising large debt facilities. Data-centre developers are searching for land, power and anchor tenants. Chip capacity remains tight. Governments are treating AI capability as strategic infrastructure.

That story is real. But it is also widely understood.

Once the infrastructure constraint becomes consensus, the investment question changes. The edge moves from recognising AI demand to understanding which parts of the infrastructure stack can actually deliver.

Demand does not automatically create value. Capacity can be delayed. Grid access can be uncertain. Cooling can become a constraint. Financing can become expensive. Regulation can shift cost allocation. Enterprise customers may not scale adoption unless security, governance and data control are in place.

The market may be right about AI demand, but still wrong about where durable value accrues.

What may be missed

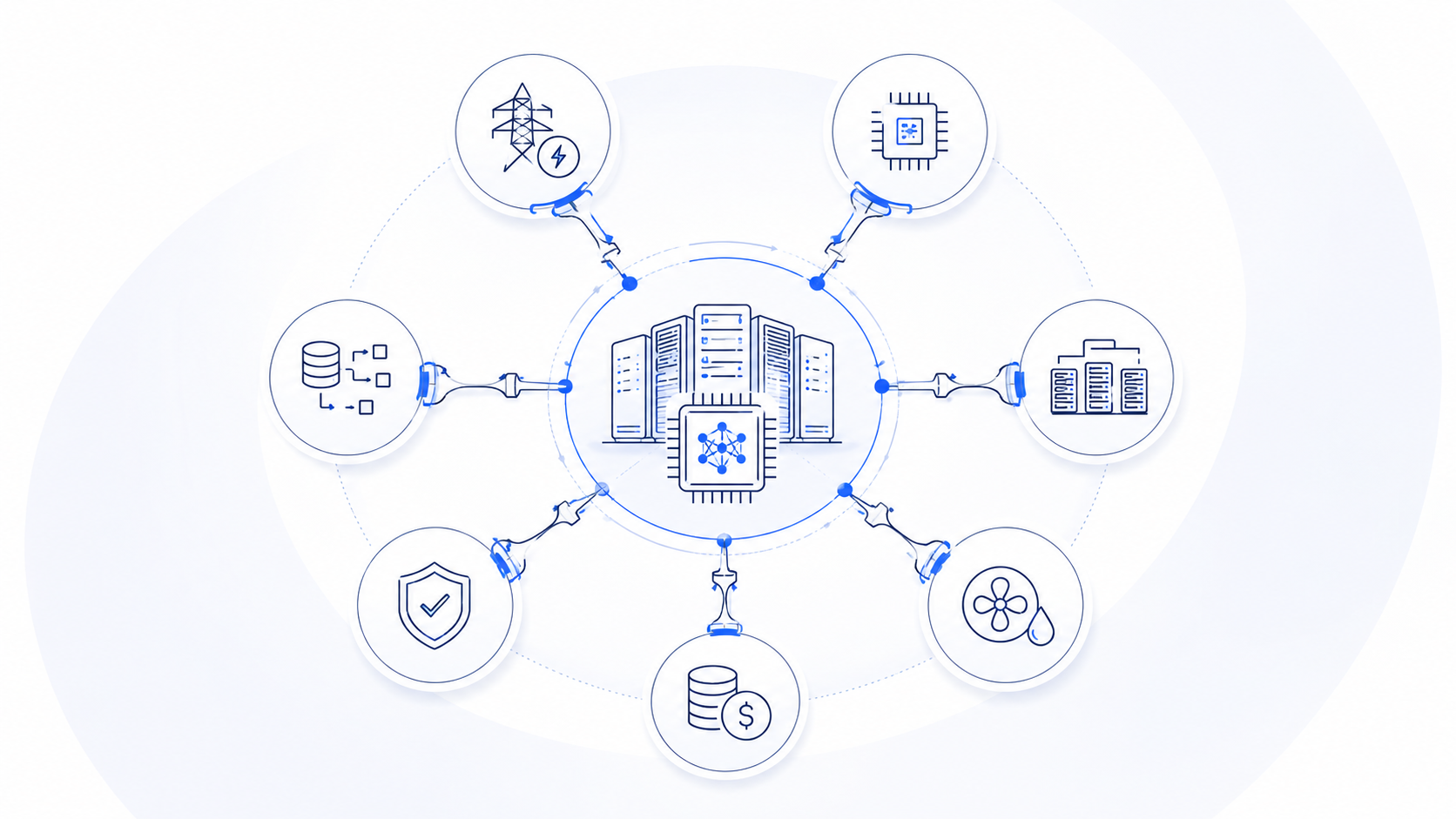

AI infrastructure is not one market. It is a chain of linked constraints.

At the physical layer sit chips, memory, data centres, cooling, land, power and grid capacity.

At the financial layer sit private credit, hyperscaler capex, infrastructure funds, sovereign capital and anchor-customer commitments.

At the deployment layer sit enterprise data, cloud platforms, agent frameworks, observability, security, governance and systems integrators.

A bottleneck in any one layer can change the economics of the others.

A data-centre project is not only a real-estate decision. It is also a power decision, a cooling decision, a financing decision, a customer-demand decision and, increasingly, a governance decision.

That is the part of the AI infrastructure story that may still be underweighted.

Why it matters

For investors and strategy teams, AI infrastructure exposure is becoming less generic.

Not every data-centre asset is equally positioned. Not every power source is equally valuable. Not every cloud platform has the same enterprise distribution. Not every AI infrastructure provider can secure chips, customers, capital and permission to build.

The better question is no longer simply:

Who benefits from AI growth?

It is:

Who controls the scarce layer that makes AI growth deliverable?

That creates both advantage and exposure.

Operators with secured power and credible grid access may be better positioned than those with only announced capacity. Cooling and power-equipment providers may benefit as thermal and electrical constraints intensify. Data platforms and cloud ecosystems may capture value if enterprise AI adoption consolidates around governed data environments. Security and governance vendors may become necessary infrastructure as AI agents move into regulated workflows.

But companies dependent on scarce chips, delayed grid connections, uncertain permitting, expensive retrofits or weak governance may face margin pressure, slower deployment or execution risk.

What to watch next

Key watchpoints include power procurement, grid-connection timelines, data-centre financing, cooling capacity, semiconductor supply, regulatory cost allocation and enterprise AI governance.

The most important signals may not be the loudest AI announcements. They may be the quieter moves that show who is securing power, capital, sites, permissions, trusted data environments and deployment channels.

The market has noticed the AI infrastructure constraint. The next question is whether it has understood where constraint becomes advantage, where it becomes exposure, and who can turn AI demand into deliverable value.