From Iran to AI: The Geopolitical Consequences for Financial Services

When geopolitical tensions rise in the Middle East, markets usually focus on the obvious variables: oil prices, shipping routes and supply disruptions.

But the escalation involving Iran may be sending a more consequential signal.

The deeper impact may not lie in the immediate shock to energy markets, but in the second- and third-order consequences for industries that depend on vast quantities of reliable electricity — and the financial institutions that fund them.

Across energy infrastructure planning, AI investment cycles and financial-sector adoption of artificial intelligence, a new pattern is emerging.

Artificial intelligence is quietly becoming energy‑dependent financial infrastructure.

The First Signal: Energy Volatility Is Returning

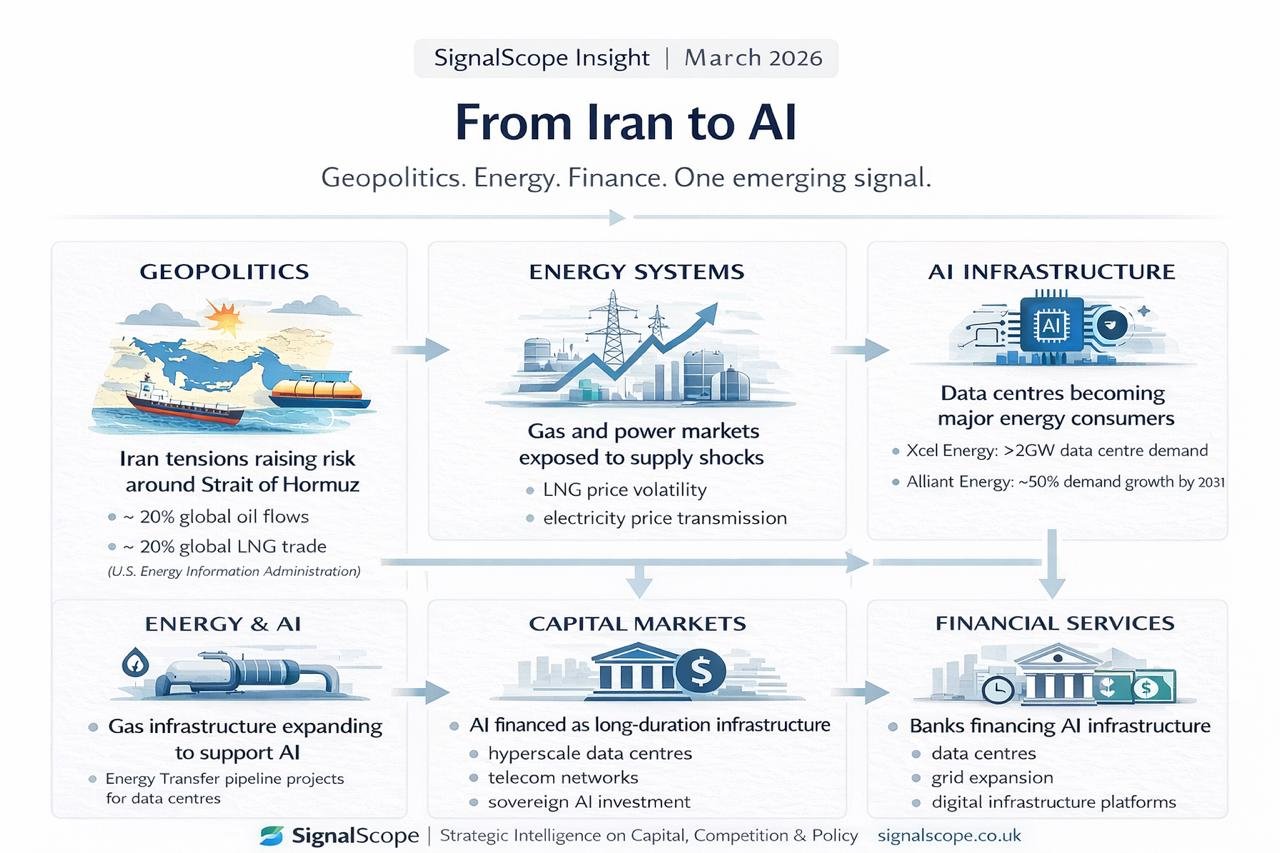

Iran sits adjacent to the Strait of Hormuz, one of the most critical energy corridors in the global system.

According to the U.S. Energy Information Administration, roughly one‑fifth of global petroleum liquids consumption and around one‑fifth of global liquefied natural gas trade pass through the Strait of Hormuz each year.

This makes the corridor one of the most geopolitically sensitive nodes in global energy markets.

While geopolitical crises in the region are often framed primarily as oil shocks, the implications are broader. Disruption to shipping through the strait can also affect global LNG flows, particularly exports from Qatar to Europe and Asia.

Because natural gas frequently sets the marginal price of electricity in many power markets, volatility in LNG supply can quickly translate into volatility in electricity prices.

And electricity demand itself is undergoing a structural shift.

Infrastructure operators are increasingly preparing for a new category of large and persistent energy demand: artificial intelligence data centres.

For example, U.S. pipeline operator Energy Transfer has announced natural‑gas supply agreements and pipeline infrastructure designed to serve hyperscale data‑centre campuses, including facilities in Texas.

The implication is increasingly clear: energy shocks no longer affect only traditional industrial sectors.

They increasingly affect the infrastructure required to power the AI economy.

The signal is subtle but important: a geopolitical event in the Gulf can now propagate through energy markets, electricity prices and digital infrastructure — before eventually reaching the balance sheets of financial institutions.

The Second Signal: The Grid Is Being Rebuilt for AI

Across recent utility earnings calls and investor presentations, a striking pattern is emerging: electricity demand forecasts are increasingly being rewritten around AI‑driven data‑centre growth.

For example:

Xcel Energy reports more than 2GW of data‑centre capacity already contracted or under construction, with an additional pipeline of roughly 4GW of potential demand.

Alliant Energy forecasts electricity demand increasing by around 50% by 2031, driven largely by hyperscale data‑centre expansion.

Utilities across multiple regions are planning gas generation, grid expansion and storage investment specifically to accommodate large AI‑related loads.

For decades, electricity demand in developed economies was largely stable.

Now utilities are preparing for the possibility that compute demand could become one of the fastest‑growing sources of electricity consumption in the global economy.

Artificial intelligence is beginning to resemble a new form of heavy industry.

The Third Signal: AI Has Become Physical Infrastructure

The idea of AI as a purely digital technology is increasingly outdated.

Training and operating large AI models requires enormous clusters of high‑performance processors operating continuously inside massive data‑centre facilities. Individual campuses can draw hundreds of megawatts of electricity, equivalent to the power consumption of medium‑sized towns.

Energy infrastructure providers are already adapting to this shift.

Utilities are developing “large load strategies” to serve hyperscale computing customers, including dedicated infrastructure and customised tariffs.

The implication is clear: AI expansion is becoming structurally linked to:

natural‑gas generation

electricity transmission networks

LNG supply chains

geopolitical energy stability

When those systems become volatile, so does the cost base of the AI economy.

The Fourth Signal: Capital Markets Are Treating AI as Infrastructure

Capital markets are increasingly financing AI expansion in ways that resemble traditional infrastructure cycles.

Across multiple signals observed in recent months, capital flows have been directed towards:

hyperscale data‑centre expansion

telecom network redesign to support AI workloads

cooling and energy‑efficiency technologies

sovereign and national AI infrastructure programmes

This suggests investors increasingly view AI not as discretionary technology spending but as a long‑duration infrastructure investment cycle.

Historically, infrastructure cycles of this scale have been closely intertwined with the financial system.

Banks finance the assets.

Asset managers allocate capital to them.

Insurers underwrite the risks.

Which means the financial sector becomes structurally exposed to the same shocks.

The Fifth Signal: Enterprise AI Is Moving Into Production

Signals across technology and consulting ecosystems suggest that enterprise AI is entering a new phase.

Consulting alliances between model developers and firms such as Accenture, McKinsey and Capgemini indicate that enterprise AI is moving beyond experimentation and into operational deployment.

At the same time, a rapidly expanding ecosystem of companies is emerging around AI governance and control layers, including:

AI observability platforms

agent monitoring and rollback systems

secure routing layers for AI traffic

governed enterprise data environments

These developments suggest that organisations increasingly treat AI not as experimental software, but as mission‑critical operational infrastructure.

Once AI becomes infrastructure, energy volatility becomes an operational risk rather than a technology risk.

The Financial System Is Now Inside the AI Energy Loop

Taken together, these signals point to a structural shift.

Artificial intelligence, energy systems and financial markets are becoming tightly interconnected.

Banks are financing the infrastructure required for AI expansion: data centres, grid upgrades, energy generation and telecommunications networks.

Asset managers are allocating capital to infrastructure funds, energy companies and digital‑infrastructure platforms that support AI workloads.

Financial institutions themselves are embedding AI across operations, risk management and fraud detection systems.

In effect, the financial system is becoming deeply embedded in the infrastructure required to power the AI economy.

That infrastructure now depends heavily on energy systems exposed to geopolitical risk.

The SignalScope Pattern

Viewed individually, each of these signals appears unrelated:

geopolitical tensions in the Middle East

rising electricity demand from data centres

AI governance platforms emerging across enterprise software

capital markets financing hyperscale infrastructure

banks embedding AI into operational processes

But viewed together they reveal a pattern.

Artificial intelligence is becoming energy‑dependent financial infrastructure.

Energy volatility therefore no longer affects only oil markets or industrial sectors.

It increasingly shapes the cost structure of the digital economy — and the financial institutions funding it.

What Financial Leaders May Need to Consider

For financial institutions, the implications may be subtle but significant.

First, rising energy volatility could introduce new cost dynamics into enterprise AI deployment. Organisations may increasingly prioritise targeted, governed AI systems that deliver clear operational value rather than large‑scale experimental compute programmes.

Second, banks financing AI infrastructure may need to reassess exposure to long‑lived assets such as data centres and energy infrastructure tied to rapidly evolving technology cycles.

Third, asset managers allocating capital to infrastructure funds, utilities and digital‑infrastructure platforms may find that geopolitical energy risks increasingly shape portfolio performance.

Looking Around the Corner

The Iran conflict is currently being interpreted primarily as an energy story.

But the deeper signal may be that the global financial system is becoming structurally exposed to the energy requirements of the AI economy.

Artificial intelligence may still be driven by algorithms and data.

But increasingly, its trajectory may be shaped by something far more fundamental:

Power, infrastructure and geopolitical stability.

About SignalScope

SignalScope is a strategic intelligence platform designed to identify early signals of structural change across industries.

By analysing developments across sectors — including geopolitics, infrastructure, regulation, capital markets and technology — SignalScope helps senior leaders understand how seemingly disconnected events combine to create new strategic risks and opportunities.

The goal is simple: to help organisations see the patterns forming across markets before they become obvious.

More information: signalscope.co.uk